A Guide To Personal Real Estate Corporation (PREC)

Are you a real estate professional looking to optimize your tax strategy while enhancing your business credibility? A Personal Real Estate Corporation (PREC) might be the solution you’ve been searching for with the help of an expert.

A PREC is a specialized legal entity that allows licensed real estate professionals to incorporate their business activities. This structure enables you to receive income through a corporation rather than personally, creating numerous financial advantages while maintaining professional standards.

Unlike standard corporations, a Personal Real Estate Corporation operates under specific regulations designed for the real estate industry. This specialized structure recognizes the unique nature of real estate professionals who typically work as independent contractors but benefit from corporate structures.

At One Accounting, we’ve helped numerous real estate agents and brokers navigate the complexities of establishing and managing their Personal Real Estate Corporation, providing them with significant tax benefits and business protection.

Let’s look at the key benefits of operating as a Personal Real Estate Corporation.

What Exactly is a PREC?

A Personal Real Estate Corporation is a corporation that provides the services of a member of a profession that is regulated by a governing professional body. Certain regulated professions are permitted to form professional corporations under their governing regulations. Realtors are regulated by the Real Estate Council of Ontario (“RECO”) and are permitted to form PRECs under TRESA.

Key Benefits of Incorporating as a PREC

When you establish as a Personal Real Estate Corporation, you gain access to several powerful tax strategies:

- Income splitting opportunities

Distribute income to family members in lower tax brackets through non-voting shares, potentially reducing your overall family tax burden. For example, if you’re in a 50% tax bracket and can distribute $50,000 to a family member in a 20% bracket, you could save $15,000 in taxes annually.

Strategic tax deferral

Retain earnings within your corporation, deferring personal income tax until you decide to withdraw funds. This allows you to reinvest pre-personal-tax dollars into growing your business or investment portfolio. If you earn $200,000 but only need $100,000 for living expenses, you can defer personal taxes on the remaining $100,000, potentially saving $30,000-$50,000 in immediate taxes.

Lower corporate tax rates

Benefit from corporate tax rates that are typically lower than personal tax rates on business income. In many provinces, small business corporate tax rates range from 9-13% compared to personal marginal rates that can exceed 50%.

Let’s also look at how you can carry asset protection.

Asset Protection Through Limited Liability

Your Personal Real Estate Corporation creates a legal separation between your personal assets and business liabilities. This structure protects your personal property from many business-related claims, providing peace of mind as you grow your real estate practice.

While professional liability for your real estate activities remains your personal responsibility, incorporating can help protect against certain contractual disputes, employee-related issues, and general business debts. This separation can be crucial during economic downturns or if your business faces unexpected challenges.

That’s not just it though! You also get enhanced professional credibility!

Enhanced Professional Credibility

Operating through a Personal Real Estate Corporation can significantly enhance your professional image. Many clients and other real estate professionals see incorporated agents as more established and committed to their business. Additionally, banks and other financial institutions often view corporations more favorably when considering financing options.

A corporate structure also facilitates clearer business branding and marketing efforts. Your Personal Real Estate Corporation allows you to build a professional brand that can outlast your individual career and potentially be transferred or sold in the future.

Let’s also look at the limited liability for PREC’s.

Limited Liability for PREC's

The difference between a professional corporation and a non-professional corporation is limited liability. If you incorporate your consulting business and you get sued, you will generally only lose the amount you invested. If you are not incorporated, you could potentially lose all of your assets.

If you are a PREC and are sued for malpractice, it will be a claim against your liability insurance. The corporation cannot protect you.

However, if you default on a loan, your assets are protected by the corporation.

Step-by-Step Process to Establish Your PREC

Got your eligibility and the legal stuff sorted? Awesome! Now let’s walk through the process step-by-step so you can get started.

Ready to set up your Personal Real Estate Corporation? Follow these essential steps:

- Consult with financial and legal professionals:

Get specialized advice from experts like One Accounting who understand both real estate and corporate taxation. This initial consultation should include a cost-benefit analysis specific to your income level and business model.

Complete a corporate name search and reservation:

Ensure your desired business name is available and complies with naming regulations. Most provinces require a NUANS report that checks for similar existing names. Your PREC name typically must include “Personal Real Estate Corporation” or “PREC” in the title.

File Articles of Incorporation:

Submit the required documentation to your provincial corporate registry. This includes details about directors, share structure, business purpose, and registered office address. Fees typically range from $200-$400 depending on your province.

Establish comprehensive corporate records:

Create minute books, share registers, and other necessary legal documentation. This includes organizing an initial board meeting, issuing share certificates, and creating corporate bylaws.

Register for required taxes:

Obtain a Business Number and register for HST/GST as needed. Determine your fiscal year-end strategically based on your business cycle and personal tax situation.

Set up corporate banking and accounting systems:

Establish dedicated financial infrastructure for your PREC, including separate bank accounts, credit cards, and accounting software. Implement systems for tracking expenses, managing receipts, and separating personal from business finances.

Notify your real estate regulatory authority:

Inform the relevant governing body about your newly established PREC. Submit any required documentation including copies of your incorporation papers and your written agreement with your brokerage.

Update your professional agreements:

Modify your agreement with your brokerage to redirect commission payments to your PREC rather than to you personally. Ensure all regulatory requirements for these agreements are met.

At One Accounting, we streamline this process by providing end-to-end support for real estate professionals establishing their Personal Real Estate Corporation.

Let’s also look at the tax planning stratergy that should be incorporated.

Tax Planning Strategy

As an unincorporated realtor, you could be subject to the highest marginal tax rate (depending on your income, can be as high as 53.53%). As a PREC, the tax rate is much lower and set at 12.5%. The additional tax savings can then be used to build your investment portfolio.

1. Tax deferral:

a. As an unincorporated realtor, you could be subject to the highest marginal tax rate (depending on your income, can be as high as 53.53%). As a PREC, the tax rate is much lower and set at 12.5%. The additional tax savings can then be used to build your investment portfolio.

2. Split your income:

a. You can pay your family members wages or issue them dividends. The catch is that, when paying wages, the wages must be for “reasonable services performed”, which means your family members must be actively engaged in the business.

b. Actively engaged is usually considered as at least 20 hours a week

3. Salary vs Dividend:

a. You have the opportunity to pay yourself either a salary or dividends. If you pay yourself a salary, you will still need to remit CPP.

b. But if you pay yourself a dividend, CPP contributions are not required, leaving you with excess cash to invest in other income-producing investments.

4. Use Marginal tax rates:

a. Canada’s marginal income tax regime means that the more money you earn in a year, the higher your tax rate will be. Lower-earning years could reduce your tax rate—which explains why it may make sense to withdraw funds during a slow year. Let's look at a comprehensive case study for the same

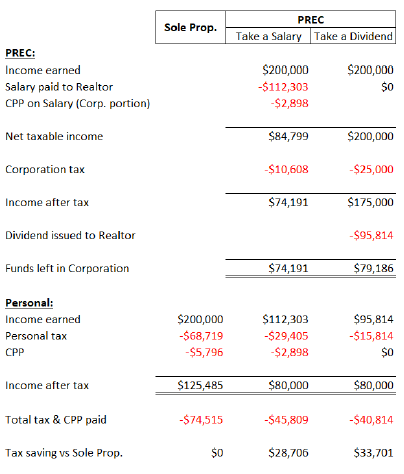

Case Study

Ms. X receives $ 200 000 in income as a Realtor during the year. Ms. X only needs $ 80 000 to maintain her lifestyle and wants to use any excess income for investing purposes. How does a PREC assist in deferring taxes?

Conclusion

A Personal Real Estate Corporation offers substantial benefits for qualifying real estate professionals, including significant tax advantages, liability protection, and enhanced professional credibility. However, proper setup and management are essential to maximize these benefits.

The decision to incorporate should be based on your specific circumstances, including income level, career stage, family situation, and long-term business goals. What works for one real estate professional may not be ideal for another.

One Accounting provides specialized accounting services for real estate professionals considering or operating a Personal Real Estate Corporation. Our experienced team can help you determine if a PREC aligns with your financial goals, guide you through the incorporation process, and provide ongoing support to ensure your corporation remains compliant while optimizing your tax position.

Ready to explore how a Personal Real Estate Corporation could transform your real estate practice? Contact One Accounting today for a personalized consultation tailored to your specific situation.

Share:

Recent Blogs

Top Tax Write-Offs for Small Businesses in Canada

10 Commonly Missed Tax Credits & Deductions for 2026

GST/HST Credit Payment Dates in Canada

What Is a Compilation Engagement?

What Is the Toronto Vacant Home Tax?

Internal auditor vs external auditors

The Basics of Accounting Services Every Business Should Know

Leya Koshy

CA — Accounting Director, One Accounting

Leya Koshy is a Chartered Accountant (CA) and the Accounting Director at One Accounting. With a strong foundation in accounting principles and Canadian tax regulations, Leya leads the accounting operations at the firm with precision and professionalism. She plays a key role in delivering accurate financial reporting, corporate compliance, and client advisory services across the firm's diverse client base. Her commitment to excellence and detail-oriented approach ensures that clients receive the highest standard of accounting support, helping businesses maintain financial clarity and confidence.

- Phone: +1 416-278-1283

- Email: [email protected]