How to Build the Best Share Structure for Your Business?

Are you wondering how to divide ownership in your growing business? Creating the right share structure can make or break your company’s future.

One Accounting helps streamline this process, ensuring your share structure aligns with your business goals and complies with legal requirements.

Let’s understand the fundamentals of shares and how they impact ownership and decision-making within your business.

SHARES

A share represents ownership in a company. When you own shares of a company, you essentially own a portion of that company. Shares are typically issued by companies to raise capital, and they can be bought and sold on stock exchanges or through private transactions.

Now that we’ve covered the basics of shares, let’s explore the role of shareholders and how they influence a business’s direction.

SHAREHOLDERS

A shareholder is an individual, institution, or entity that owns shares in a company. Shareholders are also commonly referred to as stockholders or equity owners. By owning shares, shareholders hold a fractional ownership interest in the company.

Right to vote:

Shareholders typically have the right to vote on important corporate decisions, such as the election of the board of directors, mergers and acquisitions, and changes to the company’s charter or bylaws.

Attend Meetings:

Shareholders may also attend annual general meetings to voice their opinions and concerns.

Dividends:

They may receive dividends, which are distributions of a portion of the company’s profits.

Annual financial statements:

They have the right to obtain annual financial statements of the company as soon as it is available for issuance.

With a clear understanding of shares and shareholders, let’s now look at the different share classes.

SHARE CLASSES

When structuring a business, not all shares are created equal. Different share classes can grant varying rights, such as voting power, dividend entitlements, and profit distribution.

Understanding the distinctions between share classes is crucial for aligning ownership with the strategic goals of your business.

Let’s look into different share classes and their features.

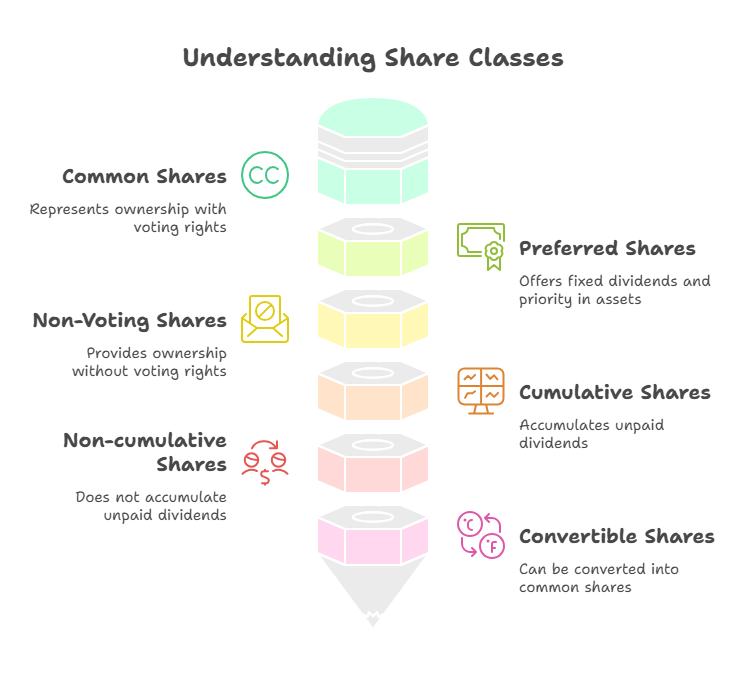

1. Common Shares/ Ordinary Shares

- The basic form of equity ownership in a company

- Typically entitles holders to voting rights in company matters

- Share in company profits through dividends, though not guaranteed

- Claim on residual assets in liquidation after creditors and preferred shareholders are paid

- Carry higher risk compared to preferred shares but often offer higher potential returns

2. Preferred Shares/ Preference Shares

- Class of shares with preference over common shares in dividends and liquidation

- Typically, they do not carry voting rights or have limited voting rights

- Offer fixed dividends at regular intervals, providing income stability

- Holders receive dividends before common shareholders

- Preference in the distribution of assets in liquidation

- Can be convertible into a specified number of common shares

- Attract investors seeking steady income with less volatility

3. Non-Voting Shares

- Shares without voting rights in corporate decisions

- Provide ownership stake without participation in governance

- Typically issued to raise capital while maintaining control for existing shareholders

- Offer dividends and potential capital appreciation similar to common shares

- Often used to attract investors seeking investment returns without involvement in company decisions

- Useful for founders or key stakeholders who wish to retain control over decision-making

- May be convertible into voting shares under certain conditions

- Commonly seen in dual-class share structures to separate economic interests from voting rights

- Provide flexibility for companies to access capital markets while preserving management control

- Can be traded on stock exchanges, offering liquidity to investors despite a lack of voting rights

4. Cumulative vs. Non-Cumulative Shares

Cumulative Shares:

- Accumulate unpaid dividends if not distributed

- Unpaid dividends accrue and must be paid before common dividends

- Assure shareholders of eventual dividend payment

- Commonly preferred by investors seeking steady income streams

- Help maintain consistent dividend payouts during lean financial periods

- Ensure shareholders receive missed dividends when financially feasible

Non-Cumulative Shares:

- Do not accumulate unpaid dividends if not declared

- Forfeit rights to dividends not declared in a given period

- Typically offer higher potential dividends compared to cumulative shares

- Provide companies with greater flexibility in managing dividend payments

- Commonly preferred by companies with uncertain or fluctuating earnings

- Offer shareholders the potential for higher returns in exchange for increased risk

5. Convertible Shares

- Can be converted into a specified number of common shares

- Provide flexibility to investors seeking potential capital appreciation

- Offer potential for participation in company growth

- Typically issued as preferred shares

- Convertibility features may be exercised at the option of the shareholder or automatically at a predetermined time or condition

- Allow investors to benefit from both fixed income and equity appreciation

- Attract investors seeking a hybrid investment with lower risk compared to pure equity

- Provide companies with a means to raise capital without immediate dilution of ownership

- Enhance liquidity and investor interest in the company’s securities

- Offer a balance between downside protection and upside potential for investors

Explore this video explaining shares and share structures in detail, covering different types of shares, voting rights, and how ownership is structured!

Now that we’ve explored the different share classes and their unique characteristics, let’s take a closer look at how they come together to form a share structure that aligns with your business objectives.

What is a Share Structure?

A share structure refers to the composition and distribution of shares within a company. A well-defined share structure is essential for corporate governance, investor relations, and regulatory compliance.

Share Structure outlines the types of shares issued, the number of shares outstanding, and the rights and privileges attached to each class of shares.

Reddit discussions are filled with entrepreneurs confused about share structure, from how many shares to issue to navigating voting rights and investor equity.

Key Components of a Share Structure

Below are the fundamental components that shape a company’s share structure and governance.

Types of Shares: Common types include common shares, preferred shares, non-voting shares, etc.

Number of Shares: Total number of shares issued by the company, including authorized shares and shares outstanding

Classes of Shares: Different classes may have distinct voting rights, dividend preferences, or conversion features

Ownership Distribution: Specifies the ownership distribution among founders, investors, employees, and other stakeholders

Rights and Privileges: Outlines the rights and privileges attached to each class of shares, such as voting rights, dividend entitlements, and liquidation preferences

Convertible Securities: Includes convertible shares, stock options, warrants, or other securities that can be converted into common or preferred shares

Authorized Capital: Maximum number of shares the company is authorized to issue as per its articles of incorporation

Treasury Shares: Shares repurchased by the company and held in its treasury, which may be reissued or cancelled

Shareholder Agreements: Any agreements governing the rights and obligations of shareholders, such as voting agreements, buy-sell agreements, or shareholders’ rights agreements

Regulatory Compliance: Ensures compliance with applicable laws, regulations, and corporate governance standards related to share issuance and ownership

With a clear understanding of share structure and its key components, let’s now explore the different types of share structures

Types of Share Structures

Companies can adopt different share structures depending on their ownership goals, governance needs, and investor preferences. Some businesses prioritize control by issuing multiple share classes with varying voting rights, while others focus on simplicity with a single-class structure.

Understanding the different types of share structures helps businesses align shareholder interests with long-term growth and stability.

1. DUAL CLASS SHARE STRUCTURE

A dual-class share structure is a system in which a company issues two or more classes of shares, each with different voting rights and privileges.

Typically, one class of shares (often designated as Class A) has superior voting rights, while another class (often designated as Class B) has subordinate or no voting rights but may have other economic benefits, such as priority in dividend payments or liquidation proceeds.

Here’s an overview of the dual-class share structure:

Class A Shares

- Full voting rights in corporate decisions

- Entitled to dividends declared by the company

- Opportunity for capital appreciation

- Freely transferable on stock exchanges

- Represent ownership stake in the company

- Subject to market risks and potential returns

- May have preemptive rights to purchase additional shares

- Typically the most common class of shares issued by a company

- Provide shareholders with a voice in company governance

- Offer liquidity and investment opportunities in the company’s securities

Class B Shares

- Typically have fewer or no voting rights compared to Class A shares

- Offer economic benefits such as dividends and capital appreciation

- May be issued to concentrate voting control in the hands of certain shareholders

- Provide companies with flexibility in structuring ownership and control

- Often used to maintain control by founders or insiders while raising capital

- Offer liquidity and investment opportunities in the company’s securities

- Generally represent an ownership stake in the company, but with limited voting power

- May have different dividend preferences or other features compared to Class A shares

- Subject to market risks and potential returns

- Commonly issued alongside Class A shares in dual-class structures

2. MULTI-CLASS SHARE STRUCTURE

A multi-class share structure is a system in which a company issues multiple classes of shares, each with different rights, privileges, and characteristics.

Unlike a dual-class share structure, which typically involves two classes of shares (e.g., Class A and Class B), a multi-class share structure may involve three or more classes of shares.

Each class of shares may have distinct voting rights, dividend preferences, conversion features, or other economic benefits.

These classes of shares may be designated as Class A, Class B, Class C, and so on, depending on the company’s preference and the specific features of each class. Each class of shares may carry different voting rights, with some classes having multiple votes per share and others having fewer or no voting rights at all.

Let’s walk through the essential steps to create a share structure that best supports your business goals and growth strategy.

Steps to Create Your Share Structure

A well-structured share system not only supports business growth but also helps attract investors and maintain governance stability. Creating an effective share structure involves the following steps:

1. Determine Your Total Shares

Start by deciding how many shares to issue. A common approach is:

- Starting with 100 or 1,000 shares for simple structures

- Using 10,000 or more shares for complex arrangements

- Keeping some shares unissued for future use

2. Assign Share Values

You’ll need to set:

- Par value (nominal value of each share)

- Issue price (what investors pay)

- Fair market value (real worth of shares)

3. Decide Share Distribution

Consider these factors:

- Founder contributions (money, time, ideas)

- Key employee incentives

- Investor requirements

- Family member involvement

- Future growth plans

Once your share structure is in place, it’s important to follow best practices to ensure it remains effective, compliant, and aligned with your business objectives as it evolves. Let’s explore the best practices for share structure.

Best Practices for Share Structure

Creating the right share structure is crucial for your company’s long-term success and growth. Following proven best practices can help you avoid common pitfalls and build a foundation that serves your small business well into the future.

Keep It Simple

Start with a basic structure that you can adjust later. Complex arrangements often lead to problems and costly legal fees.

-

Plan for Growth Reserve shares for

Future employees, new investors, business expansion, stock option plans

Document Everything

Maintain clear records of Share certificates, shareholder agreements, transfer restrictions, voting rights and dividend policies

Consider Tax Impact

Different share structures can have varying tax consequences. Your structure should minimize the tax burden, allow for tax-efficient profit distribution, support business succession planning, and enable smooth ownership transfers

With a solid understanding of share structures and their impact on your business, you’re now better prepared to make informed decisions that align with your goals and vision.

Conclusion

Your share structure forms the foundation of your business ownership. Taking time to set it up correctly now saves headaches later. One Accounting professionals are ready to help you create a share structure that supports your business goals while protecting everyone’s interests.

Want to ensure your business has the right share structure? Contact One Accounting today for a free consultation with our experienced team. We’ll help you build a strong foundation for your company’s future growth.

Frequently Asked Questions

The number depends on your business size and future plans. One Accounting can help you determine the optimal amount.

Yes, but it’s often complex and expensive. It’s better to set up the right structure from the start.

No, you can create different share classes with varying rights to suit your needs.

Yes, you can customize dividend rights for each share class based on your needs.

Different structures have different tax implications. Consult with One Accounting for tax-efficient solutions.

You’ll need articles of incorporation, shareholder agreements, and share certificates at minimum.

Yes, different share classes can have different values based on their rights and features.

Each share class may be treated differently during a sale, depending on their rights and preferences. Some classes might have priority in receiving proceeds, while others might have special conversion rights that activate during a sale.

Share:

Recent Blogs

Top Tax Write-Offs for Small Businesses in Canada

10 Commonly Missed Tax Credits & Deductions for 2026

GST/HST Credit Payment Dates in Canada

What Is a Compilation Engagement?

What Is the Toronto Vacant Home Tax?

Internal auditor vs external auditors

The Basics of Accounting Services Every Business Should Know

Leya Koshy

CA — Accounting Director, One Accounting

Leya Koshy is a Chartered Accountant (CA) and the Accounting Director at One Accounting. With a strong foundation in accounting principles and Canadian tax regulations, Leya leads the accounting operations at the firm with precision and professionalism. She plays a key role in delivering accurate financial reporting, corporate compliance, and client advisory services across the firm's diverse client base. Her commitment to excellence and detail-oriented approach ensures that clients receive the highest standard of accounting support, helping businesses maintain financial clarity and confidence.

- Phone: +1 416-278-1283

- Email: [email protected]