Comparing $105,000 Salary vs. Dividend from a Corporation

Running your own incorporated business means you have the flexibility to decide how to pay yourself, either as a salary or as a dividend. This choice directly affects your taxes, take-home income, and even retirement benefits. Many business owners in Canada often wonder which approach is better for them, especially when they earn around $105,000 a year.

In this detailed guide, we’ll break down the salary vs. dividend debate, using real numbers to help you understand what’s best for your situation.

Many entrepreneurs struggle with this choice, so let’s start by breaking down the key differences between salary and dividend income in Canada.

Understanding the Basics: What’s the Difference Between Salary and Dividend?

Before comparing the two, it’s important to understand how each form of payment works.

- Salary: Paid as employment income. It’s deductible for the corporation and taxed at your personal income tax rate. You also contribute to CPP (Canada Pension Plan) and may be eligible for Employment Insurance (EI).

- Dividend: Paid from after-tax corporate profits. It’s not deductible for the corporation, but it benefits from a dividend tax credit to avoid double taxation.

In simple terms, salary counts as an expense for your company, while dividends come from profits after corporate taxes.

Now that you understand the basics, let’s explore what happens when you decide to pay yourself a salary of $105,000.

Salary Scenario: When You Pay Yourself a $105,000 Salary

Choosing to draw a salary is a common option for small business owners who want stable income and future CPP benefits. In this scenario, the company pays you $105,000 as an expense.

Key Breakdown:

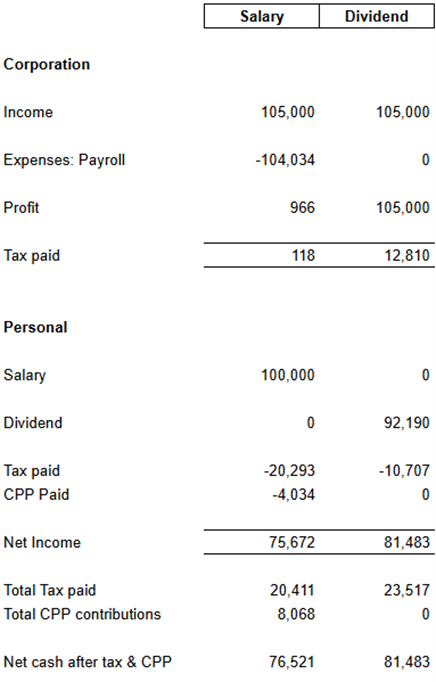

- Gross Income: $105,000

- Salary paid (Gross): $100,000 (leaving room for Employer CPP contributions)

- CPP (Employer + Employee): $8,068.20

- EI: $0 (if owner-managed)

- Corporate Profit Remaining: $965.90

- Corporate Tax: $117.84

- Personal Tax (Approx.): $20,411

After all taxes and deductions, your take-home pay is roughly $76,521.

Having explored the salary route, it’s equally important to understand what choosing dividends looks like for a $105,000 income.

Dividend Scenario: When You Pay Yourself $105,000 as Dividends

Alternatively, if you choose dividends, your company pays corporate tax first, and then you receive the remaining profit.

Key Breakdown:

- Corporate Income: $105,000

- Corporate Tax: $12,810

- After-Tax Profit (Dividend Available): $92,190

- Personal Dividend Tax (Approx.): $10,707

Your total take-home pay after both corporate and personal taxes is $81,483.

Head-to-Head Comparison: Salary vs. Dividend ($105,000)

When Salary Works Best

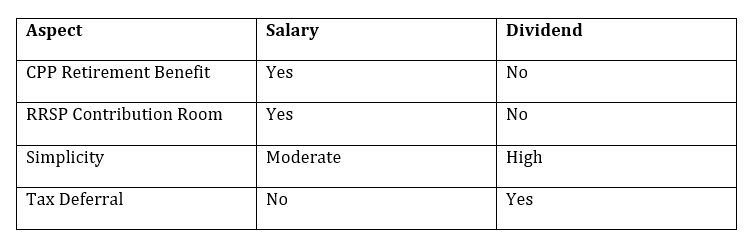

If your goal is to build long-term retirement savings and ensure consistent income, a salary is a better option.

Benefits of Choosing Salary:

- CPP Contributions: You’ll receive government pension benefits in the future.

- RRSP Eligibility: Salary creates RRSP contribution room.

- Stable Cash Flow: Regular pay makes budgeting easier.

- Deductible Expense: Reduces your company’s taxable income.

When Dividends Make More Sense

If you prefer simplicity and immediate tax savings, dividends might be your go-to option.

Benefits of Choosing Dividends:

- Lower Immediate Tax: No CPP deductions

- Flexibility: You can time dividends strategically.

- Simplicity: No payroll setup or remittance deadlines.

- Tax-Efficient Payouts: Great for retained earnings.

Since both salary and dividends have advantages, many business owners prefer a blended strategy that balances tax savings and long-term benefits.

The Hybrid Strategy: Combining Salary and Dividends

Example Hybrid Plan:

- Draw a base salary of $65,000 (for CPP and RRSP eligibility).

- Pay yourself $40,000 as dividends (to reduce overall tax).

Many entrepreneurs overlook key tax implications when deciding how to pay themselves, let’s highlight the most frequent errors.

Common Mistakes Business Owners Make

Avoiding these common errors can help you save thousands:

- Paying dividends without considering personal tax brackets.

- Forgetting that dividends don’t create RRSP room.

- Paying only salary and ignoring potential corporate tax savings.

- Not setting aside enough for personal tax on dividends.

At the end of the day, the right choice depends on your financial priorities, growth plans, and long-term lifestyle goals.

Final Thoughts: Choosing What’s Right for You

So, which is better, salary vs. dividend? The truth is, there’s no one-size-fits-all answer.

- Choose Salary if you value CPP, RRSP growth, and predictable income.

- Choose Dividends if you want immediate savings and simpler administration.

- Choose a Hybrid Approach if you want the best mix of both.

At the end of the day, the right decision depends on your personal financial goals, lifestyle, and business structure.

Why Work with One Accounting

At One Accounting, a top-tier CPA firm, we specialize in helping business owners like you make smarter financial decisions. Our experts analyze your unique situation and design a strategy that minimizes taxes and maximizes savings, whether through salary vs. dividend planning, Corporate Tax Planning Services, or Bookkeeping Services Toronto.

We combine advanced accounting technology with personalized service to ensure your business runs efficiently and profitably.

Share:

Recent Blogs

Top Tax Write-Offs for Small Businesses in Canada

10 Commonly Missed Tax Credits & Deductions for 2026

GST/HST Credit Payment Dates in Canada

What Is a Compilation Engagement?

What Is the Toronto Vacant Home Tax?

Internal auditor vs external auditors

The Basics of Accounting Services Every Business Should Know

Disclaimer: Information shared in this blog is general in nature and may not apply to all situations or circumstances. Contact One Accounting for accurate, professional advice.

Keith Jacob Noronha

CA — Accounting Manager, One Accounting

Keith Jacob Noronha is a Chartered Accountant (CA) and the Accounting Manager at One Accounting. Keith brings strong technical expertise in bookkeeping, corporate tax compliance, and financial management, supporting a wide range of business clients across Canada. As Accounting Manager, he oversees day-to-day accounting operations, coordinates client engagements, and ensures that all deliverables meet the firm's high standards for accuracy and timeliness. Keith's hands-on approach and deep understanding of Canadian accounting practices make him a trusted resource for clients navigating complex financial requirements.

- Phone: +1 647-556-1299

- Email: [email protected]