Essential Regulations for Bookkeeping in Ontario: What Every Small Business Should Know

Operating a small business in Ontario requires more than just delivering your product or service. One of the most crucial aspects of running a sustainable business is ensuring your financial records are accurate, up-to-date, and compliant with the law.

At One Accounting, we’re dedicated to helping small businesses manage their bookkeeping and financial responsibilities clearly and confidence. Our expert team uses the latest technology and tailored advice to guide you every step of the way.

1. Understanding Bookkeeping Obligations in Ontario

Staying compliant starts with understanding what’s expected of your business. Bookkeeping obligations in Ontario are governed by both provincial and federal laws, and they require accurate, timely, and organized record-keeping.

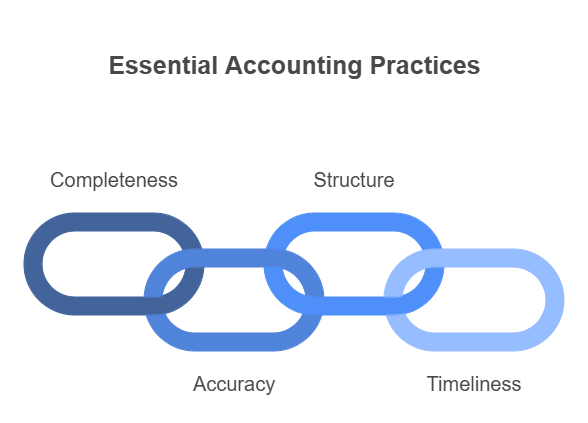

The key areas to focus on when managing your bookkeeping obligations in Ontario are as follows:

a. Legal Requirements

- Completeness: Every transaction must be recorded in full.

- Accuracy: Figures must match your receipts, invoices, and statements.

- Structure: Use a system (manual or digital) that keeps all records clear and traceable.

- Timeliness: Transactions should be entered promptly to avoid backlogs or errors.

b. Record Retention

- Invoices and receipts from both customers and suppliers

- Bank statements, loan documents, and credit card statements

- Employee pay stubs and payroll summaries

- Lease agreements, contracts, and CRA correspondence

2. HST Registration and Compliance

Navigating HST rules is a big part of Bookkeeping in Ontario, especially as your business grows. Once your revenue hits a certain level, you must charge, collect, and remit HST on all applicable transactions.

Doing this right ensures you don’t end up with unexpected tax liabilities. A few important things to keep in mind are listed below:

a. Threshold for Registration

If your total revenue (before expenses) exceeds $30,000 in any 12 months, you’re required to register for an HST number with the Canada Revenue Agency (CRA). This rule applies whether you’re a sole proprietor, partnership, or corporation.

b. Collection and Remittance

- Start collecting HST on taxable sales

- Set aside the collected amount for regular remittance

- File returns either monthly, quarterly, or annually, depending on your CRA-assigned schedule

Mistakes in HST remittance can lead to serious fines, so tracking your liabilities through accounting software is highly recommended.

c. Input Tax Credits (ITCs)

The good news? You can recover the HST you pay on business expenses through Input Tax Credits. This includes:

- Office supplies

- Software subscriptions

- Marketing services

- Professional fees

Tracking and claiming ITCs correctly reduces your tax burden and improves cash flow.

3. Payroll and Employee Record-Keeping

Once you hire employees, your payroll responsibilities begin. Managing payroll properly is one of the most important and tightly regulated parts of Bookkeeping in Ontario.

The key components to ensure your payroll and employee record-keeping meet legal and operational standards are as follows:

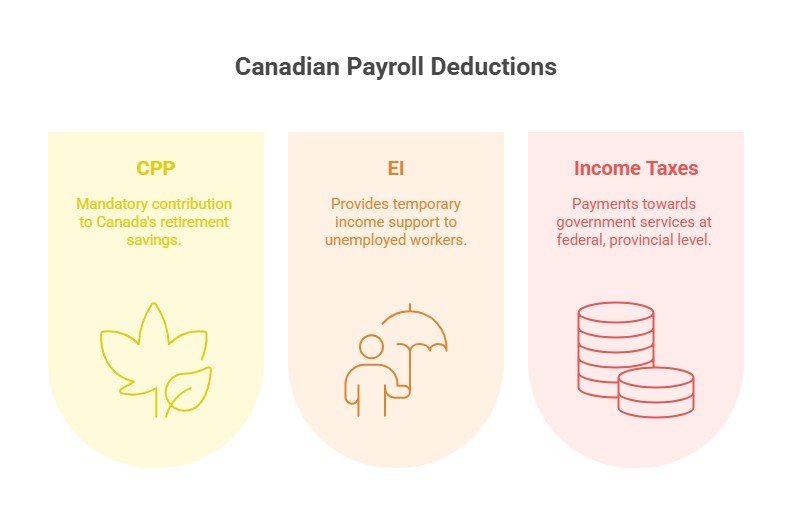

a. Payroll Deductions

- Canada Pension Plan (CPP)

- Employment Insurance (EI)

- Federal and provincial income taxes

b. Record Maintenance

Payroll records must be maintained for each employee. This includes the following:

- Hours worked and overtime

- Gross and net pay

- Vacation pay and bonuses

- Benefits, deductions, and withholdings

4. Capital Assets and Depreciation

a. Recording Assets

- Purchase date and cost

- Description of the asset and how it’s used

- Asset category (e.g., machinery, office equipment)

b. Capital Cost Allowance (CCA)

CCA is a tax deduction that allows you to write off the depreciation of capital assets over time. Each asset class has a prescribed rate set by the CRA. For example:

- Computers: 55% declining balance

- Vehicles: 30%

- Furniture: 20%

5. Choosing the Right Accounting Method

The accounting method you choose impacts how your income and expenses are reported. The right method offers clarity, accuracy, and easier tax planning.

a. Cash vs. Accrual Accounting

- Cash Accounting: You record transactions when cash is received or paid. It’s simple and ideal for small businesses with limited inventory.

- Accrual Accounting: You record income when it’s earned and expenses when incurred, regardless of payment date. It provides a more accurate picture of profitability.

b. Selecting the Appropriate Method

Sole proprietors often use the cash method, while corporations are generally required to use accrual. Consider consulting One Accounting to determine which method aligns best with your operations and compliance needs.

One common question that often comes up among Ontario business owners is: “What is the ideal legal structure for a bookkeeping practice operating in Ontario, Canada?” In a recent Reddit discussion, professionals shared their real-world experiences and advice, here’s a look at what they had to say.

Once you’ve selected an accounting method, the next step is streamlining your process with the right accounting software.

6. Utilizing Accounting Software

a. One Accounting - Full-Service CPA Firm

At One Accounting, we help clients choose and configure the right accounting tools. We provide guidance, training, and ongoing support to make the software work for you.

b. Software Options

- QuickBooks: Great for general use

- Xero: Excellent for remote teams

- Sage: Ideal for inventory-heavy businesses

c. Features to Consider

- Real-time reporting dashboards

- Automated HST tracking and remittance tools

- Integrated payroll modules

- Cloud-based access for anytime updates

7. Implementing Internal Controls

a. Preventing Errors and Fraud

- Require supervisor approval for all expenses

- Reconcile bank accounts weekly or monthly

- Lock financial periods after reports are finalized

b. Segregation of Duties

- One person handles invoicing

- Another processes payments

- A third does the monthly reconciliation

8. Preparing for Audits

Even if you’re doing everything right, the CRA may still audit your business. The best way to survive is to stay ready.

a. Audit Readiness

- Well-organized and easy to access

- Consistently updated

- Matched against filed returns

Avoid last-minute scrambling by staying ahead all year long.

b. Professional Assistance

One Accounting helps businesses prepare audit-ready books. We ensure your data is clean, your procedures compliant, and your confidence high.

Now that you understand the key pillars of bookkeeping in Ontario, let’s wrap up with the big picture and the next steps.

Conclusion

Good bookkeeping is the heartbeat of a healthy business, and in Ontario, it’s also the law. From collecting HST and handling payroll to managing capital assets and audit prep, there’s a lot to juggle. That’s why having a partner like One Accounting makes all the difference.

As a top-tier CPA firm based in Toronto, One Accounting specializes in helping small businesses simplify and streamline their financial responsibilities. Our services go beyond basic bookkeeping to include corporate tax planning, payroll management, and personal tax services.

Ready to cut bookkeeping costs? Claim your 2 months of free bookkeeping with One Accounting! Be smart and get maximum savings today.